It’s time to break the credit cycle and regain financial freedom.

What used to be cheerful spaces on r/phcreditcards or r/adultingph for swapping air-mile hacks have transformed into raw, real-time confessionals. The threads carry a distinct digital signature—high comment-to-upvote ratios tracking a communal financial panic.

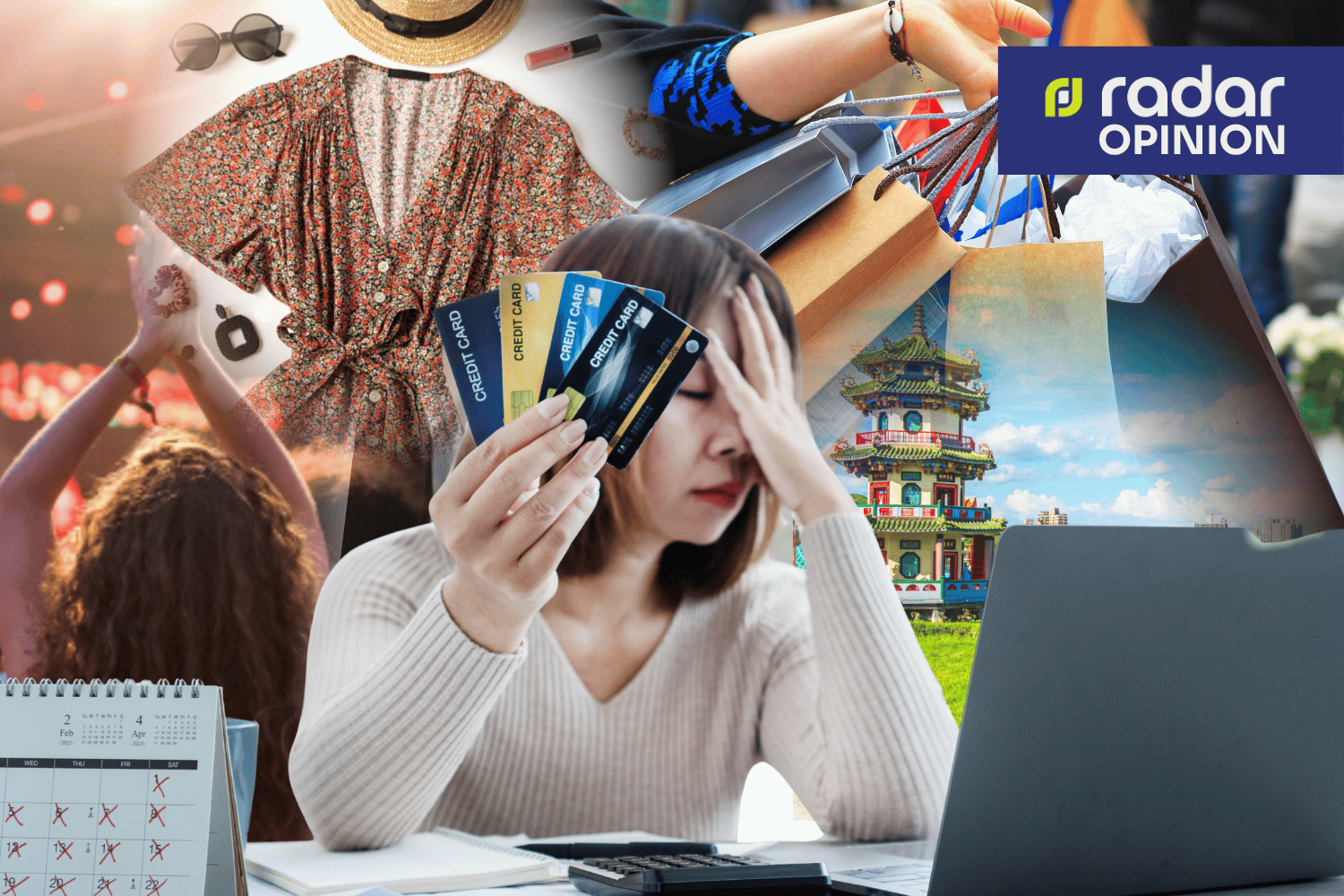

Young Filipino professionals, often earning respectable entry-level or virtual assistant salaries, are suddenly staring down debts from ₱300,000 to well over ₱1,000,000.

They didn’t buy luxury sports cars or designer goods. They simply swiped for an aesthetic lifestyle that their feeds told them was completely mandatory.

As one highly upvoted user shared on r/PHCreditCards, “I fell into the trap of thinking my ₱50k salary meant I belonged to the BGC lifestyle. It started with ₱200 iced coffees every day, then ₱1,500 weekend brunches, then a swipe for a weekend trip to Taiwan because everyone on my feed was doing it… I’m 24 and drowning.”

The algorithm rigs the game

To view this as a simple failure of willpower misses the point. The modern feed does not just entertain; it dictates a subconscious baseline standard of living.

When a young professional lingers over a “Japan Travel Vlog” or a “Quiet Luxury Café Outfits” reel, the platform’s engagement algorithm notes the attention. Within days, their feed is flooded with identical lifestyle content.

This creates an intense psychological echo chamber. When every video on a young worker’s phone normalizes high-velocity luxury spending as routine “self-care,” the credit card ceases to be an emergency financial tool. It becomes a passport to bridge the gap between their actual salary and an algorithmically generated identity.

Breaking the credit cycle

To get out of debt you have to go beyond personal shame and use a very mechanical, localized recovery strategy.

First, stop the money bleeding by opening your local banking apps (BPI, UnionBank, BDO, Maya) and toggling the “Lock Card” feature and cutting the automated subscription pipelines. Next, disconnect your credit cards from e-commerce apps to bring back vital psychological friction to buying.

Then you have to call immediately the hotline of your bank and ask for a “balance conversion to installment.” That eliminates the 3.5% compounding monthly finance charge that is so destructive and turns chaotic debt into a fixed monthly term with a greatly reduced, non-compounding interest rate.

Second, create a localized “debt avalanche” by listing all of your debts with the exact balance and interest rate owed. Pay only the minimum amount due on all cards in order to preserve your credit score.

Then, put all of your extra pesos toward the card with the highest interest rate. When that card is at zero, throw everything you were paying on that card each month at the next highest interest rate card until you are completely debt-free.

Financial maturity begins when we see distance from the aesthetic feed not as a sacrifice, but as self-preservation. Real peace of mind isn’t found in a beautifully curated lifestyle story, it’s found in a clean line and an unburdened life.

READ: